The $1 Trillion Overreaction: Why AI Agents Won’t Kill SaaS

The $1 Trillion Overreaction: Why AI Agents Won’t Kill SaaS

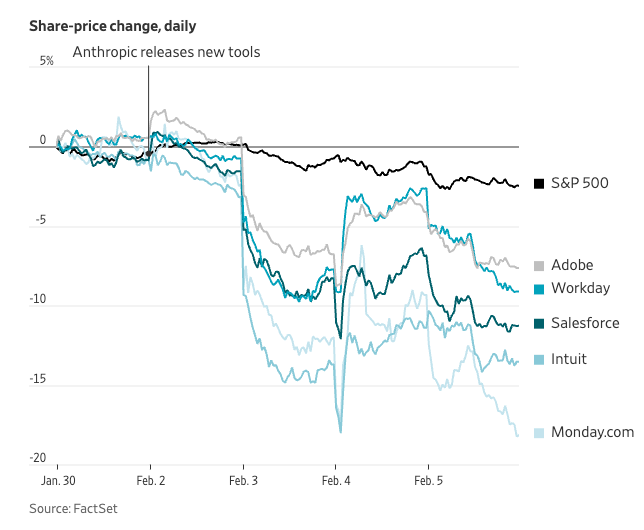

Following Anthropic’s recent agentic announcements, software stocks didn’t just stumble — they capitulated. Investors didn’t just sell; they reassessed the fundamental pace of automation. In aggregate, roughly $300–600B of market value has been erased across public software and adjacent technology sectors as investors adjusted long-term assumptions. Legal software and knowledge-work SaaS were hit first, but the pressure spread broadly across the application layer.

This was not about a single product release. It was about credibility. Agentic execution crossed a threshold where displacement risk began to feel near-term rather than theoretical. Investors did what they always do in moments like this: they moved first, before the economics were fully visible.

The market reaction is understandable. The takeaway is wrong. The simplistic narrative is that AI will replace software. The more accurate interpretation is that the SaaS model is being forced to evolve faster than the market is comfortable with.

What actually happened

Recent AI announcements from Anthropic acted as catalysts, not causes. They made it easier to imagine agents executing end-to-end workflows in categories that have historically supported large SaaS businesses, particularly in legal, compliance, and other knowledge-heavy domains.

The market reaction was broad because the concern was not feature parity. It was business model risk. Investors simultaneously questioned whether seat-based pricing remains viable, whether parts of the application layer remain defensible, and whether traditional SaaS growth assumptions still hold.

In moments like this, markets stop debating quarters and start debating trajectories.

The three forces driving the repricing

Most of the sell-off can be explained by three structural forces. Everything else is downstream.

1. Seat-based pricing and business models are misaligned with agents

As agents take on more work, the number of human users required to execute that work will decline. That creates a real headwind for traditional seat-based expansion, where revenue scales with headcount.

What changes is not the need for software, but the unit of monetization. Agents still consume compute, access data, execute workflows, and produce outcomes. Value shifts from counting users, to measuring consumption, and ultimately to pricing outcomes.

This transition is familiar. Open-source weakened per-seat license economics while expanding services and support markets. Cloud eliminated upfront licenses and replaced them with usage-based infrastructure spend. In each case, seat-based models eroded while total value capture moved to new dimensions.

Agents follow the same pattern. Seat growth slows, consumption grows, and outcome-based pricing becomes viable where value can be measured. The expansion vector shifts, not the opportunity.

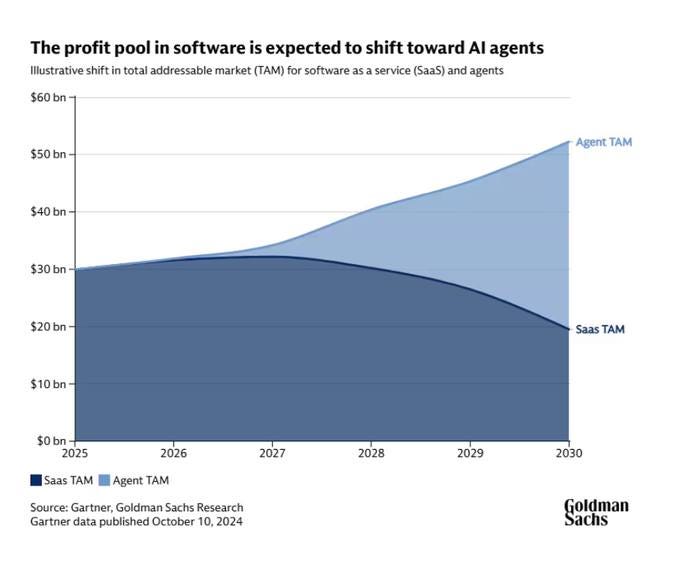

2. Perceived TAM migration from SaaS to agents

The market is implicitly assuming a zero-sum shift in TAM from SaaS to agents, with application-layer value compressing faster than vendors can adapt. ’Shallow SaaS’ — wrappers that merely summarize text or manage simple lists — is assumed to lose relevance and pricing power. What this framing misses is that a meaningful share of agent-driven value can still accrue to SaaS vendors, particularly those that evolve into agentic platforms rather than remain static applications. It also underestimates the new markets that emerge alongside agents rather than replacing existing software outright. The TAM shifts. It doesn’t disappear, and it doesn’t skip software vendors.

3. Lower barriers shift who builds, not whether software is needed

AI does not eliminate the need for durable software. It enables larger, technically mature IT teams to build more workflow-level functionality themselves, while increasing competitive intensity among software vendors serving smaller customers.

In large enterprises, this reinforces traditional build-versus-buy dynamics. Internal teams (witness the recent shift at major banks like Goldman Sachs) can now assemble targeted solutions faster. However, those bespoke agents often struggle to scale across governance, security, and long-term maintenance. In smaller companies, the effect is different. They are unlikely to build, but they will face a larger supply of vendors competing more aggressively on price.

The result is more software, not less, and greater pressure on differentiation. Incumbents with distribution and trust benefit from higher capital efficiency. Growth may moderate, but operating leverage improves. This is not an extinction event. It is a re-sorting.

What the market is missing

The market is directionally right about pressure. It is wrong about outcomes.

Pricing change does not equal value destruction

Seat-based pricing will weaken in some categories. That does not mean software companies lose the ability to capture value. It means value capture shifts to metrics that reflect agentic work: tasks completed, throughput improved, risk reduced, outcomes delivered.

The winners will be companies that can price value without turning every deal into bespoke consulting. The hurdle is attribution: In a multi-agent stack, determining which vendor gets credit for the ‘outcome’ is the next great war. That capability gap is real, and it will separate strong operators from weak ones.

Enterprise SaaS does not flip quickly

Markets move in microseconds; enterprises re-architect in decades. This latency arbitrage is the investor’s opportunity. Replacing core systems is not a UX decision; it is a governance decision.

Enterprise buying behavior is dominated by cost of failure and cost to switch. Integration debt, compliance requirements, auditability, and operational risk make failure existential and switching expensive. Even when materially better technology exists, adoption timelines stretch into years because the downside risk of getting it wrong far outweighs the upside of moving fast. That is why legacy platforms persist long after alternatives are available.

There are also entire categories enterprises explicitly choose not to build. These are areas where the cost of failure is unacceptable, the specialization required is deep, and the capability is not core to what differentiates the business. Cyber security, data protection, compliance infrastructure, and resilience sit firmly in this bucket. In these domains, enterprises buy trust, continuity, and accountability, not experimentation.

Incumbents therefore have time, but not immunity. The winners will not be those with the best demo. They will be those who can reduce cost of failure while lowering cost to switch, evolving platforms in place without breaking trust, compliance, or operations, and owning the categories customers fundamentally do not want to build themselves.

The impact will be uneven by segment

A useful way to frame the impact is to group enterprise software into three categories: systems of record, systems of engagement, and operational software. Agents pressure systems of engagement first, but they increase complexity everywhere.

Systems of record are sticky, regulated, and deeply integrated, including ERP, core financial systems, CRM, HR platforms, and primary data stores. Systems of engagement focus on interfaces and workflows such as case management, ticketing, legal workflows, and customer support tools. Operational software serves as the control plane, including security, identity and access management, policy enforcement, resilience, and observability.

As automation scales, attack surfaces expand and governance requirements rise. That makes operational and control-plane software more critical, not less. Systems of record remain durable by owning data, enforcing access, and creating the walled gardens downstream tools depend on.

TAM migrates, it does not disappear

Parts of application-layer TAM will compress as agents automate workflows. At the same time, new categories expand: agent governance, non-human identity, policy enforcement, AI security, data lineage, and observability.

New failure modes create new markets. This is the next product cycle.

Efficiency changes the investor lens

The counterintuitive point the market is underweighting is that substitution risk can also be an operating leverage event. McKinsey estimates that AI will result in a roughly 12–14% increase in EBITDA for software companies.

AI may slow top-line growth narratives while improving margin durability and free cash flow. Over time, valuation frameworks will bifurcate between fragile growth stories and durable cash compounders.

Conclusion

This was not a meme sell-off. It was a recalibration of uncertainty around how software captures value in an agentic world. But the conclusion that SaaS is structurally broken is wrong.

What is breaking are models that depend on seat growth, shallow differentiation, and static applications. The next generation of winners will price outcomes instead of users, own durable data and workflows, act as control planes for agentic work, and use AI to increase operating leverage. In every platform shift, markets hit the whole category first. They figure out the winners later. This was the category penalty. The panic is now. The winners come next.