Short reactions to what's happening in AI and enterprise software. Longer arguments live on the Blog.

Cheap to build is not the same as cheap to be right. That distinction is going to separate a lot of winners from casualties over the next 24 months.

Everyone sees the same thing. AI is collapsing innovation cycles and cost to build software. The instinct is obvious - more features, more bets, more surface area. Move like OpenAI did when it was planting category flags with browsers, video, agents, everything at once.

But OpenAI was solving a different problem. They had to define the market. That part is done.

Now the constraint shows up in a different place. Your best engineers don’t scale. Your strongest PMs don’t scale. The GTM leaders who can actually close enterprise deals definitely don’t scale. And when you can build anything, the cost of building the wrong thing actually goes up.

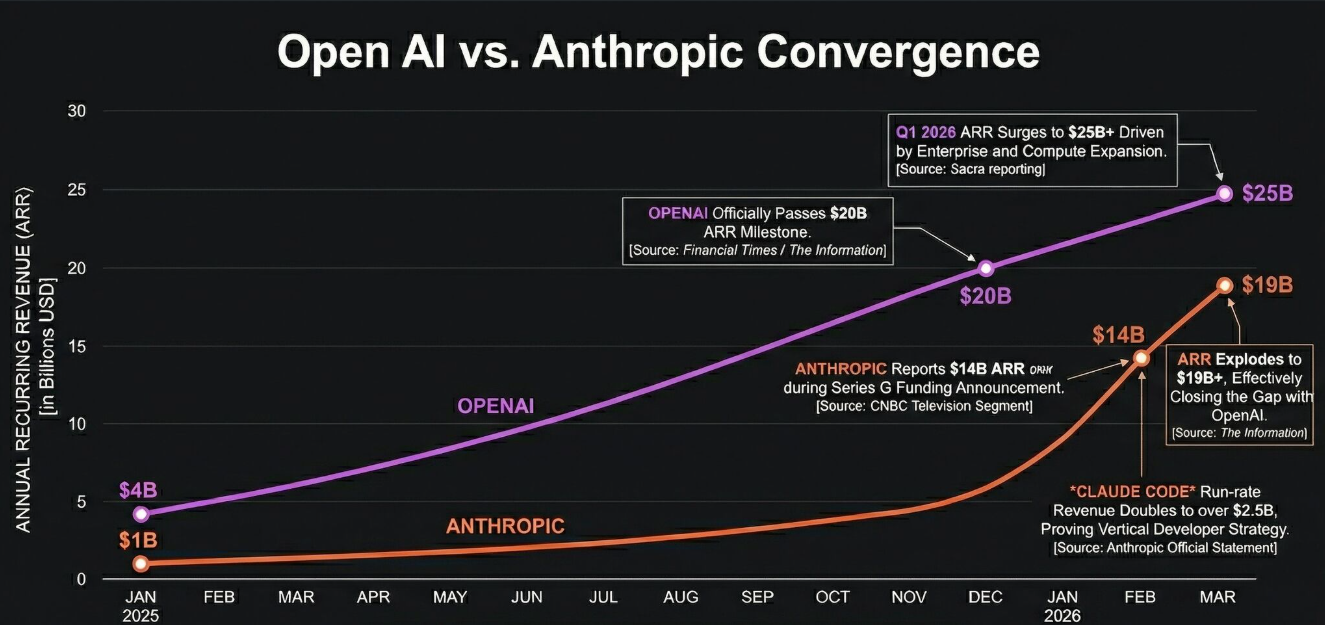

Anthropic made a different call early. They didn’t chase the whole surface. They went deep on coding and developer workflows, and built something that’s actually used in production, not just demoed.

The financial markets are already proving this out. While OpenAI was first to cross the $20B ARR milestone, Anthropic’s hyper-focused enterprise strategy just pushed them to $19B ARR in early 2026, effectively closing the gap. Their core developer tool, Claude Code, is reportedly driving a $2.5B run rate entirely on its own.

That’s not a niche. That’s a moat.

The next phase of AI-native software won’t be won by teams doing the most. It’ll be won by teams willing to cut more than feels comfortable - and go deep enough that switching away actually hurts.

The hard part was never building. It was always deciding what not to.

Nvidia is building NemoClaw. An open-source AI agent. To compete with OpenClaw.

I'm not surprised.

OpenClaw didn't invent the AI agent. It created the template - packaged it correctly and just made it feel real. But it also exposed the risks - rogue agents deleting emails. Malicious skills. Meta banning it company-wide.

Now everyone wants to build the "safe" version. The enterprise version. The better version.

But here's what I keep coming back to: in this game, distribution is the moat.

Nvidia has credibility. Open source is smart. But when Anthropic, OpenAI, Microsoft and Google bring agent orchestration to market at scale - they're not just bringing a product. They're bringing trust, enterprise relationships, and in many cases the cloud and OS stack underneath it all.

The forks and alternatives will keep coming. The experimentation is real and valuable - it's how the risks get stress-tested before the real wave hits.

Until then - enjoy the deluge.

https://www.worthview.com/nvidias-nemoclaw-explain...

AI

OpenAI’s move to kill ChatGPT’s 4o AI model saddened loyal users, but the model also has been criticized for being overly sycophantic and tied to cases of chatbot users developing psychotic delusions https://www.wsj.com/tech/ai/chatgpt-4o-openai-3151... via WSJ

AI

Spent some time playing with OpenClaw this weekend. I understand the excitement. Not because of the AI, but because of the packaging.

Four takeaways:

(1) Experience is the breakthrough

What feels like “magic” is really the modality: how agents run, how they interact through messaging, and how they plug into SaaS applications and packaged skills. It’s structured packaging that makes execution feel natural instead of brittle. That last mile matters.

(2) This is the operating template for agents

Not demos or copilots. Real systems that can do real work, run close to the data, and tap into proprietary skills and integrations. Less prompt work. More infrastructure and composition.

(3) Pricing pressure will show up quickly

Execution layers and agent runners are moving toward commodity. Wrapping them and trying to monetize the wrapper alone won’t hold. The defensible value is higher in the stack: workflows, integrations, governance, and outcomes.

(4) Security and safety are the next big questions

There are still open gaps around security, safety, and governance. That’s not a side issue. As agents move from experiments into production, these gaps will turn into new product categories and buying decisions.

Feels like the beginning of a real platform shift.

Your 2026 Infrastructure Budget is Obsolete.

DRAM prices are projected to double this quarter. This isn't a typical cycle; it’s a structural revaluation of global silicon.

The "Why": Fabs are practicing "wafer triage." To meet AI demand, they are cannibalizing standard DRAM production for High Bandwidth Memory (HBM) at a 3:1 ratio. Every AI chip produced effectively kills the supply of three "regular" memory chips.

The Implication: Your routine server and PC refreshes are now in a direct bidding war with global AI hyperscalers for the same limited silicon.

In this allocation-led economy, the "Memory Winter" will likely persist through 2028. If you haven't re-baselined your infrastructure costs yet, you’re already behind.

Full story here: https://www.theregister.com/2026/02/02/dram_prices...

AI

Hardware

SpaceX acquires xAI in a massive merger to build orbital data centers! Tackling AI's insane power demands while fueling Mars missions. This changes everything for space & tech. Details here: https://techcrunch.com/2026/02/02/elon-musk-spacex...

AI

Snowflake + OpenAI is a signal: LLMs are becoming ubiquitous, embedded, and hard to differentiate. The real battleground is shifting to data gravity, governance, and workflow integration. AI won’t win standalone - platforms will.